The present value of money is explained with real-life examples in this week’s session of Darwin’s MBA Mondays (click for all topics). If you don’t routinely perform present value versus future value comparisons, the relevance and importance may not be at the top of your list of things to focus on when making decisions. However, as noted below, everyday we’re confronted with circumstances where people or companies will seek to exploit the present value of money – and consumers’ lack of knowledge on the topic, to boost their bottom line. A personal favorite trick I’ve encountered personally on numerous occasions is when someone pushing a mortgage acceleration MLM scheme or someone in the mortgage industry says, “But you’ll save $50,000 in interest payments ….”. This “savings” is complete nonsense – don’t be fooled. I’ll show you why – by understanding the present value of money in the right context.

Present Value of Money Explained

First, let’s understand the concept of present value at its most basic level, then we’ll get into more detail. Since we tend to live in inflationary environments at all times (even though the government claims to be fearing deflation at the moment), financial models always assume something will cost more in the future than it does now. For this reason, people and businesses make calculations about whether they should defer a payment into the future or spend the money now. When possible, financial outlays are deferred when possible. $100 today is worth more than $100 in a year. If I need something a year from now, I’d sooner keep the $100 and invest it, with $104 to show for it in a year and just pay the $100 then.

You should always be thinking of money in terms of today’s value vs. future value – and not confusing the two.

Taking this a bit further with some real math and assumptions involved, one key consideration is what is your interest rate assumption is. I like to consider what is my “assumed rate of return/risk-free interest rate” or “inflation” or some other measure when considering what my money would be worth TODAY if converting from future dollars or vice versa. For simplicity, let’s assume we’re talking in terms of assumed inflation of 3%.

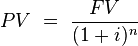

PV = Present Value

FV = Future Value

i = interest rate (percentage, or 0.03 in our example)

n = number of periods (let’s use years for simplicity – and note: interest rate must be an annual rate too then).

So for example, if someone’s talking about paying you a lump-sum payment of $100,000 in 30 years, it may sound like…about a hundred grand! But that money’s only really equivalent to about $41,000 in today’s dollars using a very conservative inflation interest rate. If you’re more aggressive with your assumptions and use say, the 8% you think you could make in stocks long term, then you’re talking just $10K! That’s right – if you can reasonably make 8% over a long period of time, that $100K in the future isn’t really that impressive. In excel, here’s what that equation looked like:

=100000/(1.08)^30

In essence, under this 8% and 30 year example above, if I were confronted with the option of either taking $15,000 today or $100,000 in 30 years, I’d take the money now!

This emphasizes just how important it is to consider what your interest rate is and the decay effect time has on money when discounted back to present dollars.

Present Value of Money Examples in Real Life

- Mortgage Acceleration Programs – I was approached once by a co-worker pushing a scammy “money merge account” which was some useless software that basically told you to pay your mortgage early. I could do that without software, but for this privilege which would give me the “discipline” to do so and use some hocus-pocus with a desperate account, I’d pay like $3000 up front and then make pre-payments to my mortgage. The guy touted how given my mortgage, I’d save something like $50,000 in interest payments off my mortgage! Sounds great right? No, it’s silly. My mortgage rate is already 4.625% and with the mortgage interest deduction, it’s probably an effective rate of about 4%. I could reasonably earn more than that with even a moderate mix of stocks and bonds over 30 years. Additionally, when I joked with him about what the Future Value of that $3,000 was, he looked bewildered. The answer? It’s well into the 5 figures for a reasonable interest rate. So, if he wants to talk Future Value by touting 50K over 30 years he should also talk Future Value for the fee for this dumb system. Or vice versa. I’d argue that the benefit from this system is present dollars is ZERO minus the $3K. At its simplest level, it only makes sense to pre-pay your mortgage if you don’t think you can earn more than the effective interest rate you’re paying on it. To sell such a move with “interest payment savings” spread across an obnoxious 30 years is disingenuous. It’s ignoring the present value of that $50K value, it’s ignoring tax deductions and it’s ignoring what the same money would have earned invested in another vehicle.

- Retirement Planning Estimates – I ran a pension analysis tool at work a while back. I don’t recall the exact number, but let’s say the projected lump sum at retirement was $1 Million. That sounds like a lot of money, right? Well, the first thing I did was to discount that number back to present dollars. $1 Million is completely arbitrary if you’re not talking in terms of present dollars. So, if I’m 25 years from retirement and my interest rate is say, 6%, that $1Million is really only worth $232K – certainly not enough to retire on! Assuming a 4% drawdown of principal of your nest egg in retirement, you’d have to plan on living off $40K per year. Since that’s well below our current annual income, that would be problematic. Of course, there’s Social Security (or what’s left of it) and other investments – but someone in my shoes might be lulled into complacency thinking about how they’re going to retire a “Millionaire”, when really, it’s only a Quarter-Millionaire in today’s dollars.

These are just a few examples of routine situations we encounter if life that require some critical thinking and assumptions to figure out what the true present value of money is, as opposed to quoted future dollars or cash flows. Without discounting future dollars back to present day dollars, you may be lulled into a foolish investment or purchase.

{ 20 comments… read them below or add one }

This was one of my favorite lessons in Finance class in college. It’s so powerful and I’ll never forget that a dollar today is worth more than a dollar in the future.

Glad you enjoyed – and brought back some enjoyable college memories! Beer…

I was always aware of the concept but never had a formula to assist in figuring out what we’ll need tmrw to live like we do today.

Thanks for the real life examples. So you’re against paying down mortgage then?

Not necessarily – if you’re a very conservative investor and consider that a good use of funds (and the peace of mind in paying off early), that’s fine. What I abhor is the disingenuous claims of these early payoff schemes touting “interest savings” without regard for present value.

You are right! In my case, I want my mortgage paid off by the time I retire (6.5 years). I am maxing out my 403B, IRA and Roth IRA. The alternative investment choice is not an issue for the $100 per month additional principal reduction. This could change, if my income significantly changes.

I’ve written dozens of posts on the mortgage acceleration scam.

My favorite dialog with one agent selling the product – I asked “would you fund a 401(k) where your deposits were 100% matched by the company, or use the funds to pay down your mortgage?” The reply was that $1 sent to your mortgage immediately saves you nearly $5 in interest, but $1 to the 401(k) ‘only’ gets you one dollar to match. The decision is a no-brainer.

Indeed. So I told the agent that if we were to ignore time value, that the $3500 paid for the software was really $1.7 million, as I could deposit that money into my kid’s Roth account and in 65 years at 10% return, it would be worth that much. Agent said I was ignorant. No, I just showed that I know how and when to use the time value of money. Equating a return over 30 years to an immediate 100% match is beyond ignorance, it’s innumeracy.

Don’t you love how obnoxious and aggressive these “associates” are? They are knowingly pushing a useless scam – shameless.

” … when I joked with him about what the Future Value of that $3,000 was, he looked bewildered” heh heh, you went and talked fancy to him, got him all twitterpated.

Good post, I enjoyed the refresher and reminder.

Wouldn’t it be nice if there was no inflation, but long-term deflation?

I used to think about life without inflation but deflation appears to be even worse (Japan). Since things are worth less in the future, people defer purchases, which wrecks the economy. Layoffs ensue, wages drop, it all goes to hell. Kind of like our current economy, but worse.

I guess that would depend on time preference and needs. I defer purchases of electronics all the time, knowing that better values and/or prices are down the road. “Early adopters” don’t really care, they want it *now*. At work, our company has benefited from falling labor costs, as fabrication shops slash margin rates in order to secure scarce work. I place orders *now* because project deadlines have to be met, even knowing that lower prices might/could be had in near future. I think that long-term deflation, same as long-term inflation in the order of 2 to 3 percent, would be natural in an economy with a stable currency and improving productivity and efficiency.

The present value thing is why I would not dump everything on the mortgage. In the back of my mind, I have the same thoughts as you when people talk about what a ripoff the interest is (yes, it is a ripoff compared to not paying any interest at all, but you do have to look at the time value of money). However, I have said that I would highly consider paying down on an accelerated schedule, but the reasons for doing this would be twofold:

1) Lowering debt means the debt is retired earlier, and your expenses drop significantly once that happens. Not everyone wants to pay debt until their 50s and 60s.

2) Paying down the mortgage has an entirely different risk factor. Sure I can invest in the markets but the more money I put in there, the more I’m exposed to that particular risk profile. Paying down the mortgage is a guaranteed return not only against current interest rates, but against future interest rates as well (I am on a variable rate, and even if I weren’t, Canadian fixed rates generally renew every 5 years).

I don’t want to be overweight house, so I think I’ll start accelerating the payments once the house declines to maybe 20-30% of net assets.

I agree, risk-free return is an important factor when considering “investments”. If mortgage rate is appreciably high, say, 6%, I’d take a 6% risk-free return over an 8% return with market risk any day.

Darwin – I have to say, I went to school full-time for an MBA, and it was a tremendous experience all around and I learned a lot. That said, the single most useful and practical concept I learned was the present value concept. Most people don’t even think about this when considering future nest egg calculations, and I just shake my head. You did a nice job here in explaining it.

Present value calculations are absolutely crucial in planning for retirement. The question about whether or not to pre-pay on your mortgage is an interesting decision as well. I have heard that it can be useful to pre-pay in the event that it gives you a lot of emotional relief to see your mortgage going down fast.

Oh no…. memories of Corporate Finance class from b-school 🙁

This post has been included in this week’s Cavalcade of Risk:

http://notwithstandingblog.wordpress.com/2011/01/25/cavalcade-of-risk-123-exam-season/

Please let your readers know.

Thank you!

Hi, Darwin,

I didn’t realize that mortgage acceleration schemes had gone MLM. As I recall the first one I saw was offered by Russ Whitney. Of course he was charging too much, but it wasn’t an MLM deal.

You might want to mention to people who do want to pay their mortgages off early — don’t make partial prepayments. That is, don’t add $50 or whatever on to your amount of mortgage’s monthly amount. Or pay those extra payments.

The one part of Russ Whitney’s spiel that made sense to me (perhaps banking professionals will dispute it) is that the finance company’s computer’s are not set up to deal with adjusting your interest and principal every month based on these partial payments. You may not even get credit for them. And that was long before we knew how many mortgages are repackaged into mortgage backed securities.

Instead, make your full mortgage payments on time every month of course, but place that $50 or whatever you can afford into a money market account. Unlike the mortgage acceleration programs, you’re not locked into making exactly two extra payments per year. Save up as much as you can afford, but no more.

You’ll earn a little extra in interest (okay, very little, but it’s something). And it’s liquid. It can double as your emergency fund. If you need it, tap into it.

Which brings up another point those mortgage acceleration programs don’t mention. If you really need to draw on your home’s equity because of losing your job, you won’t get a home equity loan. The banks want you to take out those loans only when you have the income to repay them.

Anyway, when that fund is large enough to pay off the principal you owe, then you can send them a cashier’s check to cover it 100%.

The same advice goes for people trying to pay off car loans.

If banks have a blank on their forms for where you can add extra principal on your monthly mortgage payment and they do not do the math correctly to give you proper credit for additional payments it seems to me they could be on the hook for fraud and a nice payoff for some lawyer interested in taking all similarly situated mortgage holders on in a class action against the lender.

“don’t make partial prepayments”

Sorry Rich, I disagree. The servicing company has to apply the principal prepayments correctly, and one can easily track their balance to hold them to it.

With savings/checking rates so low, if one has one other debt and is interested in paying the mortgage quicker this is the way to do it.

In this day and age of spreadsheets and finance calculators, there’s no excuse to not track ones payments. One can have a 30 yr mortgage, pay it with the payment for a 15 year amortization and know if their situation changes, they can cut back to the normal payment. 15 years of saving the extra funds at 1% will put the borrower pretty short of being able to write the 100% check as you suggest.

{ 7 trackbacks }